I am sure you have come across many advertisements asking you to invest in US Stocks from India. In today’s post, we will bust some myths about investing in US stocks and some very important steps you should take before investing in the US. In the end, you will also know some of the best ways to invest in US Stocks and the correct way to invest in US stocks. Please remember that this post is not about investing or not investing in US Stocks but informing you about things you should know before you start investing in US Stocks.

Top 10 myths about investing in US Stocks

Let’s discuss the most talked myths about investing in US Stocks. Remember these points are applicable to small investors like you and me. Most of the points concern the hidden and other fees & taxes. In the end, I will analyze each point by using a paper investment case of $2000 which I think is a reasonable amount for a retail investor trying to invest in the US market.

- 4% profit from the inflation just by simply investing in US stocks.

- Higher return in the US market than the Indian market.

- You can invest in US stocks as low as $1.

- Easy deposit and withdrawal for investing in US Stocks.

- No commision investing in US Stocks.

- Much larger market than the Indian market.

- More space for diversification options in the US market.

- Simple tax regime for capital gains from US market.

- US is a more stable market than India.

- You don’t need to invest in time analysing on US market.

Now, let’s discuss all of the points one by one.

4% profit from the inflation just by simply investing in US stocks.

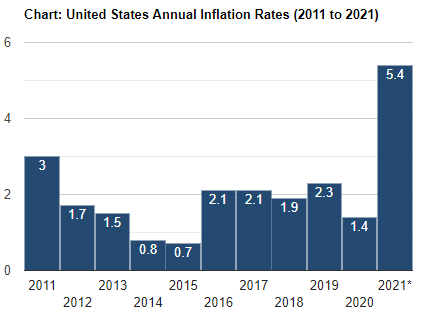

One of the biggest myths about investing in the US market is that you will get a 4% return by simply keeping the money in USD instead of INR. This is either highly exaggerated or misleading. Below are the inflation data of the US and India and you can see the inflation spiked for the US as compared to India. As you can see the inflation rate of India increased from 4.7% to 6.2% while the US increased from 1.4% to 5.4%. Before the Chinese Virus came, the inflation rate of India has been stable for the last 6-8 years. The difference in the inflation of the two countries doesn’t give a 4% return.

One may argue that it is about the increasing USD to INR value rather than the raw inflation data. Even considering this, the numbers don’t add up. In the photo below you can see the change of USD to INR over the past several months. Over the past years, the rate of change remains around 2-3%.

Let’s say none of my opinion about this is correct and you, as a retail investor, get a 4% return just for sitting on your USD instead of INR. There are so many small fees involved that will eat up more than your 4% return. We will discuss these fees in the subsequent points. Keep reading to know full details about this. Basically, you will hardly get the 4% bonus return as stated by many gurus on the internet.

Higher return in the US market than the Indian market

There is no such thing as a higher return in a market than in another market. It all depends on what you are investing in. Generally, it is referred to the comparison of return rates on the indices i.e. S&P 500 and Nifty 50. If you dig deeper the average return of S&P 500 over the last 30 years is 10.99%, 20 years is 5.90%, and 10 years is 14.70% while Nifty 50 has a return of 12.2% over the last 30 years (almost 30 years), 8.7% in the last 10 years.

Even though these historical data don’t predict the future, we can compare them and can see the trend. If you see the last 30 years NIFTY 50 has a higher return but if you check over the last 10 years, S&P 500 is out-performing the NIFTY50. If you are an investor, generally it is a long-term game and you should think for the long-term prospects. The higher return for the last 10 years gets eaten up in the fees.

I will analyze the fees in full detail with example money. Keep reading to know more. Also, the Indian market is rapidly developing while the US market is generally considered a stagnant market. You can see a higher return on a rapidly developing market even though the US is a much larger market than India.

You can invest in US stocks as low as $1

Yes, brokers like Groww, INDMoney offer you the ability to buy fractional shares as low as $1. You can absolutely buy them but how much percentage return of that $1 will you need to cover the selling fee and a good return? This is the whole game. You can sure invest as low as $1 but for real meaningful investment, you will need a substantial amount of money. You will know this when you read the example which I will cover later in this post.

Easy deposit and withdrawal for investing in US Stocks.

By easy deposit and withdrawal, you are expecting a process like normal deposits in Indian investment in UPI or net banking. It is nothing like that. You have to add a US account number. Send the amount you want and wait for 4-10 days for the amount to be credited minus the fees from both sending banks to receiving bank. The same process goes for the withdrawal. I keep saying fees and fees. It is the fees that are eating the chunks of the profits.

No commision investing in US Stocks

Yes, delivery stocks are no commission but when you sell, there will be regulatory charges and other fees just like in India. These fees are significant if you are starting to invest from $1. Yes, you can invest with no commissions but know the other fees before investing.

Much larger market than the Indian market

Technically it is true but what will be the benefit for you by investing in the much larger market? Do you have enough time to analyze another much larger market economy, the news, and most importantly, do you have enough cash to tap in those benefits.

Do you know that a broader selection pool complicates your decision-making process? More importantly, you are a lone soldier novice retail investor analyzing a completely unknown foreign market to you. If you think, you can do it, then you can for sure step on the US markets.

More space for diversification options in the US market

Diversify, don’t put all your apples in a single basket are some of the most heard phrases in the investment world. Also, I am sure you haven’t heard, put your half apples in 100 different baskets. What is the point of diversification when you don’t have enough money and reduce your return rates? Most retail investors like you and me don’t have large sums of money sitting around in our bank accounts.

Simple tax regime for capital gains from US market

You might have heard that the US and India have a Double Taxation Avoidance Agreement (DTAA) and this makes taxation on US stocks much simpler. But these are as not simple as you think it is. Your CA may and most probably will charge more by hearing the words investing in foreign markets. If you are starting with a small amount, the capital gains might not even cover your CA fees.

US is a more stable market than India.

The growth rate of the US economy is lower than India even though the size of the market is much larger than India. However, the US market is no stable market. Every economic fallout or major dips in the market all over the world starts with the US. Remember, 2008-2011, it all started in the US. Sometimes, it is much more beneficial for you to stay invested in India.

You don’t need to invest in time analysing on US market

Anyone saying that you can invest in any market without analyzing the market is lying to you. This applies the same to invest in US markets. You must study the details about the market, sector, and the specific stocks whether it is in India or the US.

Myths of investing in US market with an example for retail investor

So, enough of talking about this and that, let’s jump in with an example. Let’s say you have a total of $2000 to invest in the US market which is around Rs. 1,48,581.70 as of 18-08-2-21. For the simplification of calculations, let’s take it as Rs. 1,50,000 which I think is a reasonable amount or even much more than a retail investor can invest one time.

Now, your bank will charge you around Rs. 1000 just for sending the money. With this, you are left with Rs. 1,49,000.

At the time of writing this post, the ICICI forex exchange rate for USD is around Rs. 76.5 approx. For Rs. 1,49,000 is approximately equal to $1947.71. Another 3.5% will be charged from that exchange rate.

0.035*76.5=2.6775. Now, your effective exchange rate including the exchange fees will be 76.5+2.6775=Rs. 79.1775. Now your 1,49,000 becomes only $1881.85. Another $11.85 will be reduced as GST. $1870 is the amount you will receive in your broker wallet to invest.

Start investing in US market using$1881.85

First, this part is a little complicated but hang tight and read carefully. Let’s assume that you have chosen 7 stocks to invest in with an equal weightage of $267.14 each. Suppose you keep investing in these companies for 3 years. After 3 years 2 of the stocks is giving a loss of 20% and you are selling it.

Returns on losing stocks + dividend

This gives a total loss of 2*267.14*0.20= $106.856. On top of this, an exchange fee of 0.02 is charged which is 0.04 for the two sell orders which give you -$106.82.

During the last 3 years, you received a dividend of 2% on average on both stocks. This makes you earning 2*2*3=12%. Remember, it is a simplified calculation, you were supposed to reinvest the dividends and also the losses are over the years so, your invested amount doesn’t remain the same as $267.14 each.

Of the 12% dividend, 25% tax is deducted by the US which is 0.25*12=3% which makes your effect dividend of 9% for the period of 3 years.

Now, the total dividend over the 3 years for the 2 stocks is 0.12*267.14=$32.06-0.25*32.06=$24.05. Total return after 3 years for the 2 stocks is -106.82+24.05= -$82.77.

Return on winning stocks + dividend

Now the remaining 4 stocks you are getting a 50% gain over the last 3 years. Remember, I am considering a 1:2.5 risk-reward ratio which is above the average of 1:2, and also a winning percentage of 5/7=71.43% which is also well above the average which is widely considered to be around 60%. So, I am assuming you are performing above average which is very difficult for a new retail investor in a new market.

The total profit from the sale of 5 stocks is 0.50*5*267.14=$667.85. 667.85-0.06(exchange fee)= $667.79 A 20% flat tax is applicable as long-term capital gains (LTCG). 667.79-0.2*667.79= $534.232. Remember, you might be able to recover the losses on the LTCG but for this, you will need a good CA.

Similarly, a 2% dividend rate for the 5 stocks over the 3 years minus the 25% tax gives you a total return of 0.02*5*3*267.14 – 0.25*0.02*5*3*267.14=80.14-20.04=$60.11. The total return of the 5 stocks is 534.232+60.11= $594.34.

Withdraw Money from US Markets to Indian Account

Finally, you are getting an overall return of 594.34 – 82.77 = $511.57 from the $2000 investment. Now, you are requesting a withdrawal of 2000+511.57. For brokers like Groww, it charges $9 per withdrawal which makes a total balance of 2511.57-9=2502.57.

The bank will charge you about 10-25 dollars. Let’s take it as $12. Now, your Indian bank will receive around $2490.

As of writing this post, ICICI’s exchange rate for receiving is around 73 rupees with a 3.5% exchange fee + GST. 2490*73-0.03*2490*73-0.18*0.03*2490*73= 1,81,770-5453-982 = 1,75,335.

So, finally, you got 25,335 in 3 years when you invested 1,50,000 which is a 16.89% gain in 3 years. But this was supposed to be 30%. This gives slightly more than 5% return per year which is far less than the average return of S&P 500.

Instead of investing in US markets in the hope of getting a higher return, alternative investment platforms like the TradeCred and GripInvest will give a higher returns. I have written a detailed review of the TradeCred invoice discounting and GripInvest lease financing.

Are you ready to invest in US Stocks using Groww, INDMoney, etc.?

After seeing the above example, I think you will think again before you start investing in US Stocks. Some of you may say that some of the stocks may give a 500% return and all of the 7 stocks are profitable. If we start on this road, then, there is also a possibility of going all the 7 stocks to -80% in one month.

All I want to say is that the above example is taken as an example that is well above the average return and wins rates. You should be really careful on stepping your feet on another market especially when you are not able to maintain your domestic market portfolio.

Remember you are the small fish in the pond and big fishes always eat most of the small fishes.

Some of the fees are fixed costs so minimizing transactions and transactions in big amounts will reduce your fees in terms of percentage.

But also remember, you don’t have large sums of money, and investing a lump sum money one time increases your risks.

The price difference of the buying and selling of USD to INR eats a major chunk of your money. So, keeping in the US account and reinvesting will reduce your fees.

How to properly invest in US markets using Groww and INDMoney?

By now you know the risks and other factors which are not so nice about investing in US markets. If you are still interested in investing in US markets, then the following points may help you a lot.

- First you need to sign up on either Groww or INDMoney. Click here to sign up on Groww, activate your Demat account and get Rs. 100 for free. Click here to sign up on INDMoney and get 1000 INDCoins which you can invest in cryptocurrencies.

- INDMoney requires you to have at least 650 credit score. The Indian Demat accounts are different from the US trading accounts.

- After you finish signup up, go to the US stock sections. The US stocks are available only on desktop for Groww.

- Provide all the details and submit your application. Wait for the activation.

- Once your account is activated, add money by following the onscreen instructions.

Invest US Stocks in mutual funds

I personally use this method instead of directly investing. Instead of analyzing all these markets, stocks, news, all the fees, etc. I just do a SIP on mutual funds that invests in US Stocks. I invest in Mutual funds using Groww App.

I invest in Motilal Oswal S&P 500 but there are other funds with much higher returns. I am planning to switch to another fund. Some popular ones are ICICI Prudential US Bluechip Equity Direct Plan-Growth, NIPON India US Direct-Growth Plan, Parag Parikh Flexi Cap Fund Direct-Growth Plan, etc. You can check each one of them in the Groww App.

Always look for the fees, exit load, and expense ratio. The Parag Parikh one has the lowest expense ratio but it is a mixture of Indian and US stocks. All others have a higher expense ratio. Even though you might think that the difference is not even a percentage point, the compounding effect over a long period will be very significant.

Some more points you should remember before investing in US Markets

- Don’t invest more than 20-25% of your whole portfolio in the US market. For example, you are investing Rs. 100, your US investments should not be more than Rs. 25.

- Invest in large sums of minimum 5,00,000 only in proven tech companies which you know is not a bubble. This also means you are investing a minimum of Rs. 20,00,000. But at this point, you are not a regular retail investor.

- Make sure you are following US politics, markets, major foreign policy fallouts, US news, domestic employment news, trade wars, etc. if you are investing in US politics.

- Don’t do small deposits and withdrawal frequently.

- You are not allowed to trade in Futures and Options.

- You are not allowed to trade in intraday.

- Short-sale, GTT orders, and other advanced features are not available.

- Remember the fees, Tax, exchange fees, GST, etc.

If you are an investor or trader, you must be using Trading View. If you don’t know what is TradingView, then you should know about it. The premium features are very good and having a premium version of TradingView is very helpful for you as a trader or investor. I have written a blog post on how to get the TradingView Pro for free in India. Click here to know-how.

My Favorite Stock Trading/Investment Tools

TradeCred Review – Best Invoice Discounting Platform In India?

Best stock brokers for beginners in India.

Smallcase subscriptions for free.

Best broker and mutual fund investment for beginners – Groww – Click here to signup, activate your Demat account & Get Rs. 100 for free.

Best stock brokers for day trading –Upstox, Fyers.in (Free account, Free AMC)

Best charting platform – TradingView.com

Trusted Forex broker for Indians – Exness.com (Zero swap charges).

Become a crorepati just by investing 5k per month in mutual funds.

Busting the myths of investing in US Market.

How to increase your credit card limit temporarily?

How to invest during a market crash?

Why you should never use PhonePe to invest in Mutual Funds.

Invest in Indian startups using TykeInvest.

Disclaimer

Disclaimer: All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment’s past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit. Any ideas or strategies discussed herein should not be undertaken by any individual without prior consultation with a financial professional for the purpose of assessing whether the ideas or strategies that are discussed are suitable to you based on your own personal financial objectives, needs, and risk tolerance. This website expressly disclaims any liability or loss incurred by any person who acts on the information, ideas, or strategies discussed herein. The information contained herein is not, and shall not constitute an offer to sell, a solicitation of an offer to buy or an offer to purchase any securities, nor should it be deemed to be an offer, or a solicitation of an offer, to purchase or sell any investment product or service. Everything discussed here is only for educational purposes. Do your own research before investing.

3 thoughts on “Busting The Myths Of Investing In US Stocks For Retail Investors”